11 December 2024

Outlook for cattle farming in 2025

As part of the Teagasc Outlook 2025, Economic Prospects for Agriculture, Jason Loughrey and Kevin Hanrahan of the Agricultural Economics and Farm Surveys Department, Teagasc, forecast the expenditure for various input items and the beef price that is most likely to prevail in 2025.

They also provided a forecast of the incomes from the production of cattle in 2025.

Feedstuffs in 2025

Global cereal and oilseed futures market prices point to no change in feed prices in 2025. An 11% reduction in the volume of feed used on Cattle Finishing enterprises is forecast for 2025. Our forecast is for an average 8% decrease in overall feed volume used on Single Suckling enterprises in 2025. These forecasts are based on the assumption of normal weather conditions in 2025.

Fertiliser in 2025

Given the developments in global supply and demand, the outlook for international fertiliser prices in 2025 is for the price of fertilisers to be slightly lower relative to 2024. In our 2025 forecast, we forecast that total expenditure on pasture and forage by Irish cattle farmers will be slightly lower relative to the 2024 level.

Electricity and fuel in 2025

Fuel costs in 2025 will depend mainly on the evolution of crude oil prices. Current futures prices suggest that crude oil prices will decrease in 2025 relative to 2024 prices. Our forecast is that fuel prices in 2025 will be similar to those paid in 2024.

Other direct and fixed costs in 2025

The cost of labour is forecast to increase by 3% in 2025. However, on the average Irish cattle enterprise hired labour costs are very small and inflation in labour costs is not expected to have a major impact on overall costs of production. We forecast an increase in other direct costs of 2% in 2025. This is mainly attributed to a forecast increase in veterinary costs. Other overhead (fixed) costs are forecast to be 1% higher in 2025.

The outlook for cattle and beef markets 2025

Ireland exports close to 90% of its beef production (CSO 2024). Conditions in markets to which Irish beef and cattle are exported largely determine Irish cattle prices; though supply developments in Ireland can cause Irish cattle prices to deviate from export market prices over the short run.

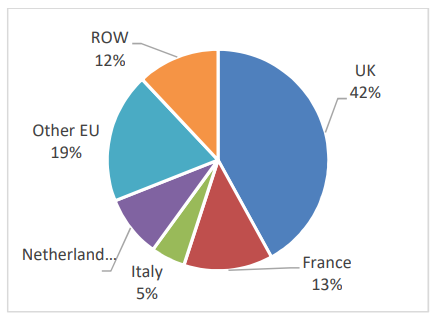

Figure 1 illustrates the destinations of Irish beef exports in 2024 (year to the end of August). The UK remains the most important export destination for Irish beef with a current export share of 42%. The importance of the EU in Ireland’s beef exports is also evident from Figure 1.

Figure 1: Estimate of Irish beef export markets by volume in 2024

Source: Eurostat COMEXT, January to August (2024)

France remains the EU member state with the highest export share of Irish beef exports at 13%. Exports to the Netherlands and Italy remain important with export shares of 9% and 5% respectively. The share of exports to the rest of the world (ROW) remains significant at 12%.

In recent years, there has been a notable increase in the volume of exports to EU markets including France. However, both consumption and overall imports of beef have declined in France during 2023 and 2024 (L’institut de l’élevage, 2024). The European Commission reports that the consumption of beef is declining in the EU-27 (European Commission 2024). At the same time, beef production is also declining in many EU member states, which counters the negative effect of reduced demand.

In many Western European countries, consumer prices for beef appear stable or increasing slightly in 2024 (INSEE France 2024a, 2024b; Federal Statistics Office Germany 2024; Statistics Netherlands 2024). In the UK, the rise in beef steak prices continued in early 2024 and remained stable through the rest of the year (Office for National Statistics 2024).

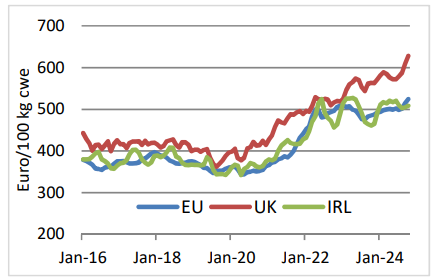

Figure 2 shows a comparison of beef prices in Ireland with the EU and UK. Figure 2 shows that beef prices in the UK continued to increase during 2024. The AHDB reports more detailed statistics according to UK region (AHDB 2024b).

Figure 2: Monthly EU, UK and Irish Finished Cattle Prices 2016 to 2024 (Excl. VAT)

Source: DG Agriculture and Rural Development, AHDB and ECB. Ireland and UK Steer R3, EU27 Young Bull R3

It is clear from Figure 2 that UK steer prices have tended to exceed Irish steer prices for most of the period. The preference among UK consumers for beef sourced in Britain provides one explanation for this long-run pattern.

However, the gap between UK and Irish prices (October 2024) significantly exceeds the long run average of approximately 10%. Given the extent of interdependence between the UK and the beef sector in Ireland, we may therefore anticipate some partial convergence in British and Irish beef prices over the coming months.

In the short run, the outlook for prime beef supplies in Ireland are determined by the current inventories of animals aged 1-2 years. Data from the Department of Agriculture, Food and the Marine (DAFM) AIMS database provide insights into developments in these inventories. Inventories for animals aged 12-24 months of age are significantly lower relative to the levels observed 12 months previously. Overall, we forecast a 4% decrease in prime beef production for 2024.

In the rest of the EU, supplies of cattle for slaughter in 2024 are likely to be lower than 2023. Overall EU production of beef in 2025 is forecast to be 1% lower in 2024 (European Commission 2024c). In the UK, the inventories for animals aged 12-24 months of age appear lower in June 2024 relative to June 2023 (DEFRA 2024b). This points to a decline in UK beef production during 2025.

In the medium term, inventories of breeding animals are the key determinant of future beef supply. Figure 3 illustrates the recent trends in dairy and beef cow inventories in the EU (readers should note the different scales on the left and right axes). In anticipation of the abolition of EU milk quota in April 2015, the numbers of dairy cows in the EU increased, however low levels of profitability in many member states subsequently reversed this trend.

Figure 3: EU27 Cow Numbers 2008 – 2023

Source: Own elaboration based on Eurostat (2024)

Dairy cows account for approximately two-thirds of the stock of cows in the EU. Under the CAP, many Member States have coupled direct payments related to both numbers of dairy and suckler cows and these policy measures will tend to mitigate some of the impact of on-going low levels of profitability on cow numbers. Beef cow numbers declined in 2023 in many EU member states including Ireland, France and Spain. Dairy cow numbers declined notably in France and Germany in 2023 and to a lesser extent in some other EU member states. Poland is an exception where the number of dairy cows increased strongly in 2023.

In the UK, there are notable declines in the size of the breeding herd and particularly for non-dairy cows. This points to some further contraction in UK beef production in the medium-term (beyond 2024).

Our forecast is for a 4% increase in the annual average finished cattle price in 2025 relative to the annual average in 2024. This equates to a price of approximately €560/100kg (including VAT) for the average R3 steer.

In 2025, a decrease in some input prices is expected to impact positively on Cattle Finishing enterprises. A rising demand for the purchase of younger cattle can emerge due to the expected contraction over the medium-term in beef production in the EU and the UK. A slight improvement in margins earned on the Cattle Finishing enterprise will further support this demand. Our forecast is that prices for weanling and store cattle will increase by 2% and 4% respectively in 2025 relative to the 2024 levels. Gross output for the average Single Suckling enterprise is therefore forecast to be higher relative to the estimated 2024 levels.

Outlook for beef enterprise net margins in 2025

In 2025, the evolution of the net margin on cattle farm enterprises will be influenced by cattle sales, cattle purchases and input expenditures.

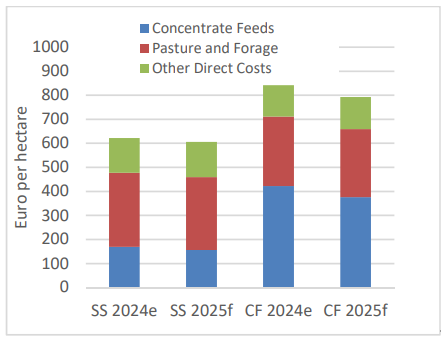

Figure 4 compares the estimated and forecast average direct costs per hectare in 2024 and 2025 for the Single Suckling and Cattle Finishing enterprises. On both enterprises, the level of expenditure on pasture and forage is expected to be slightly lower in 2025 relative to 2024. This is mainly due to the forecast of a slight reduction in the price of fertiliser.

Concentrate feed prices are forecast to be unchanged in 2025 relative to 2024. After significant increases in 2023 and 2024, the quantity of concentrate feed usage on Cattle Finishing farms is forecast to decrease by 11%. This forecast is based on the assumption of normal weather conditions in 2025. Expenditure on concentrate feed is forecast to be 11% lower on Cattle Finishing enterprises and 8% lower on Single Suckling enterprises in 2025.

On a per hectare basis, the direct costs are forecast to decrease by 3% on the average Single Suckling enterprise and by 6% on the average Cattle Finishing enterprise.

Figure 4: Estimated Direct Costs for 2024 and Forecast Direct Costs for 2025

Source: Author’s Estimates 2024 and Forecasts 2025

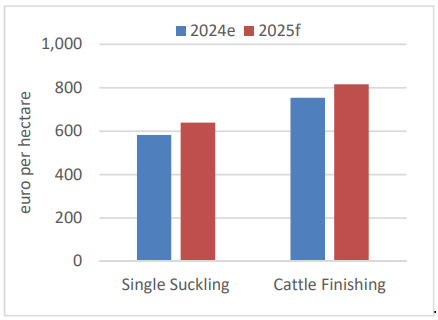

Figure 5 shows the estimated gross margin on both cattle enterprises in 2024 and the forecast gross margins for 2025. For 2025, the gross margin for the average Single Suckling enterprise is forecast to increase by approximately 10%. On a per hectare basis, the gross margin for the average Cattle Finishing enterprise is forecast to increase by approximately 8% in 2025.

Net margins on average Cattle Finishing farms are forecast to be higher in 2025 relative to 2024 with a forecast average net margin of €191 per hectare. Net margins for the Single Suckling enterprise are forecast to improve in 2025 relative to 2024. A positive net margin per hectare of €133 is forecast for 2025.

Figure 5: 2024 Gross Margin for Single Suckling (SS) and Cattle Finishing (CF) Enterprises and Forecasts for 2025

Source: Author’s Estimates for 2024 and Forecasts for 2025

The above article by Jason Loughrey and Kevin Hanrahan of the Agricultural Economics and Farm Surveys Department, Teagasc, was adapted for use on Teagasc Daily from the paper titled: ‘Review of Cattle Farming in 2024 and Outlook for 2025’ and first published in the Teagasc Outlook 2025, Economic Prospects for Agriculture.

For further information, access the full Teagasc Annual Review and Outlook 2025 publication here.

References cited in this article are available to view in the full publication.