Profitability levels rise on DairyBeef 500 farms

Alan Dillon, DairyBeef 500 Manager, examines the costs an margins witnessed on DairyBeef 500 demonstration farms over 2025.

The beef price rise of 2025 was not forecast, at least not to the degree that it did; average prices rose nearly €2/kg carcass weight across the year, coming to an average price of €7.14/kg carcass weight up from an average of €5.18/kg in 2024.

Couple this with what was quite a reasonable year weather wise – with no major upsets with regards excessive rainfall for the main grazing season – along with a slight dip in the main variable costs such as feed, fertiliser and milk replacer of between 4 and 8%, and you had what turned out to be quite the perfect year all-in-all.

Calf purchase price rose for the DairyBeef 500 demonstration farms by an average of around €60/head for beef-sired bull and heifer calves to €257 and €219, respectively, while Friesian bull calves rose to €97 per head. Most of these calves would have been purchased at between 2 and 3 weeks of age.

The Commercial Beef Values (CBVs) of the beef calves purchased have also increased in line with national figures. Beef-sired calf CBVs increased to €134, while the Friesian CBV has reduced slightly to -€4. This means that the average calf bought on the DairyBeef 500 demonstration farms in both dairy beef and Friesian calves are 3-star for CBV within their individual category.

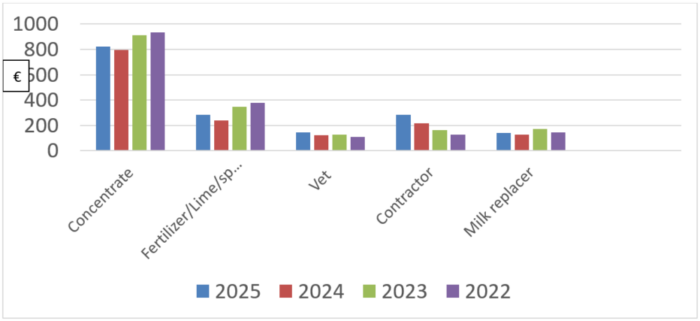

Costs on DairyBeef 500 farms

The main variable costs on the DairyBeef 500 demonstration farms are concentrate, milk replacer, vet, fertiliser and contractor charges.

While feed and fertiliser fell from their peak when input prices were at their highest in 2022 and 2023, the cost per hectare of these two big inputs did rise slightly despite the price per tonne dropping in 2025.

This is somewhat explained by farmers taking advantage of the higher beef prices and feeding extra concentrates to drive cattle into bigger weights, while extra money was invested phosphorous (P), potassium (K) and lime in 2025 after a few years of curtailed investment due to the high cost of fertiliser.

Contractor charges have been rising steadily over the past few years and, with labour being a scarce commodity on part-time farms, a higher proportion of machinery work is being carried out by agricultural contractors, and it is expected this cost will remain high in the future.

Milk replacer and vet costs have experienced more modest rises over the years. However, with the price of calves rising in 2026, it is expected that more may be spent on pneumonia vaccination programmes this year to ensure no setbacks.

Table 1. Main variable costs on DairyBeef farms 2022-2025

Farm margins

Net margins across the DairyBeef 500 farms rose substantially because of changes in the marketplace. Net margins on the demonstration farms rose to €1,465/ha (excluding subsidies and direct payments) across the group. This is a 104% increase in profitability versus the previous year.

While the increase in profitability is substantial, what is noticeable is the difference between the top third and bottom third of the monitor farms. While the bottom third had an average net margin of €666/ha, still a very good figure compared to where beef profits had been, the top third had net margins of €2,246/ha.

The top third of farmers had higher levels of output per livestock unit, higher stocking rates, and a lower level of variable costs per kg liveweight produced on the farm. The top third of farmers had total variable costs of €1.38/kg liveweight (€2.76/kg deadweight) versus €1.62/kg liveweight (€3.24/kg deadweight) on the bottom third of farmers. The top third of farmers had a stocking rate of 2.36 LU/ha, while the bottom third had a stocking rate of 1.85 LU/ha. The top third had liveweight output per LU of 592 kg compared to 562kg for the bottom third.

While the timing of sale of cattle last year could have influenced the level of profit with the price in January differing from the price in April by almost €2/kg deadweight, the main factors that influenced the level of profit achieved on calf to beef farms was output per livestock unit and stocking rate. Those farms that had their output levels on the farm maximised were in a very strong position in 2025 to make gains when beef prices rose.

Table 2: Profitable increase across DairyBeef 500 monitor farms 2023-2025

| Year | Output (€/ha) | Variable costs (€/ha) | Gross margin €/ha | Fixed costs (€/ha) | Net profit €/ ha excl. direct payments |

| 2025 | 4,181 | 1,870 | 2,311 | 846 | 1,465 |

| 2024 | 3,405 | 1,856 | 1,548 | 831 | 717 |

| 2023 | 3,330 | 1,990 | 1,341 | 799 | 542 |

Table 3: Profitability difference between top third and bottom third of DairyBeef 500 Monitor farms in 2025

| Category | Output €/ha | Variable costs €/ha | Gross margin €/ha | Fixed costs €/ha | Net profit €/ha excl. direct payments |

| Top third | 5,130 | 1,916 | 3,214 | 968 | 2,246 |

| Bottom third | 3,085 | 1,664 | 1,421 | 755 | 666 |

Threats for 2026 to calf to beef producers

While the threat of a beef price cut is always something being floated about to farmers, there has definitely been less talk of it in the past 12 months than farmers are used to. The only real issue worrying calf to beef farmers currently is calf price. While it is very hard to gauge this year where calf prices will level off at, it is fairly certain they will be higher than they started off in January last year. Once beef prices remain north of €7/kg most farmers will be in a fairly strong position come year end especially those that have their farm costs under control and remain focused on the main performance indicators of grass utilisation, herd health and buying good genetics at value.

For more on the Teagasc DairyBeef 500 Programme, visit here.