As part of the recent Teagasc National Beef Conference, Rupert Claxton, Meat Director of Gira Consultancy and Research, examined the global supply and demand for beef and presented an outlook for 2026. Below is his paper:

Background

Globally, the supply of beef is tight, and demand from the consumer is remarkably robust. The major cattle production countries are all supplying less beef to the global market in 2025 than in 2024.

A significant shortage in the US, as the drought conditions in key cattle regions continued into a third year, has led to an increase in beef exports to the US from their immediate neighbours (Mexico and Canada), but also from other key exporters, Australia, New Zealand and Brazil. Indeed, Brazil is still shipping to the US even with a 76% tariff in place.

Export availability from the leading exporters is tight. Australia is expected to be able to maintain current high volumes of production, but not grow. Brazil’s cattle cycle has turned, and production will decline in 2025 and 2026, whilst the EU cattle herd is in long-term structural decline.

Global beef price overview

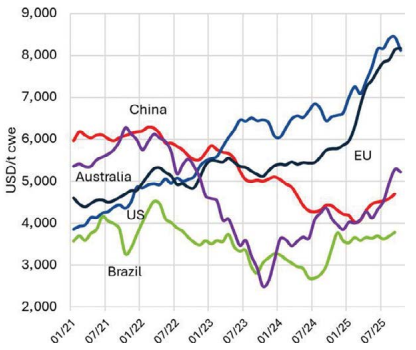

The result of good global demand and tight supply is the high prices seen today (Figure 1). This has been exacerbated at the farm gate by competition between slaughter plants for cattle as supplies tighten.

Figure 1: Key cattle producer prices in the main cattle production regions – monthly. Source: Gira.

On the other hand, the consumer has been shielded by competition in the supply chain, which limits retail price increases. There are, however, signs that this isn’t sustainable; slaughter plants are not filling their lines, and retailers have passed a higher share of the price rises through to the consumer, but not all of it yet.

More specifically, within the European market, beef prices have climbed sharply, on top of already high 2024 levels. High prices in the first half of 2025 pulled slaughter cattle forward as farmers looked to capitalise, which exacerbated the shortage in the second half of the year, a fact clear in Irish slaughter numbers today.

This has driven prices higher still. For the consumer, higher prices have now been realised on the retail shelf, and this has led to lower purchase volumes for beef, although, being more positive, the total spend on beef has increased.

Teagasc Beef Specialist, Catherine Egan spoke to Rupert Claxton at the Teagasc National Beef Conference, watch the below video for a summary of his key insights:

Implications for exports of Irish beef

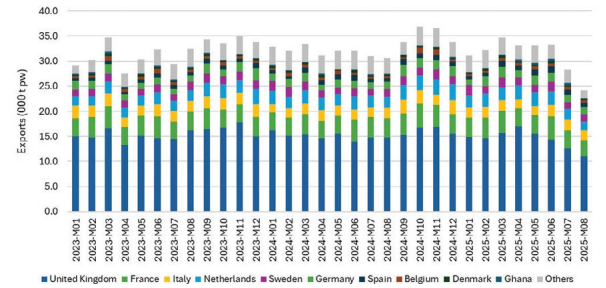

The impact on Irish beef exports is clear; reduced production is limiting the availability for exports (Figure 2), and exporters need to choose where they place volumes and how they compete.

More significantly are the potential long-term impacts of high prices. The major UK retailers are a key market for Irish exporters, and UK consumers have, for a long time, associated British and Irish beef as a core category.

Figure 2: Irish beef exports (monthly). Source: Gira based on TradeMap

However, key retail customers are looking at other major beef exporting regions for alternatives to Irish beef. Over the summer of 2025, several retailers tried fresh beef from a variety of non-European sources on their retail shelves. So far, these products have been trials; they are the market-testing alternative suppliers, learning how it could work, and building resilience in their supply chains. The risk for Ireland is that once these sources are proven, they will more readily compete with Ireland.

Rupert Claxton, Meat & Livestock Director GIRA, and Teagasc Regional Manager for Clare and Galway, Pat Clarke at the National Beef Conference 2025 in the Raheen Woods in Athenry Galway. Photo:Andrew Downes, xposure.

Summary

- Globally, the supply of beef is tight and demand from the consumer is remarkably robust.

- The result of good global demand and tight supply is the high prices seen today.

- Several UK retailers have included beef from a variety of non-European sources on their retail shelves during 2025.

- The outlook for 2026 is a continuation of the current trend, both in Europe and globally.

- Ireland is well placed to produce more beef in a way that is both environmentally and commercially sustainable.

- There are opportunities for investment in the beef sector but rationalisation at industry and farm level is needed to deliver efficiencies.

Outlook

The outlook for 2026, at least, is a continuation of the current trend, both in Europe and globally. Beef supplies remain tight, and prices will remain high. Whilst the mid-term outlook globally is for a recovery in beef production, it is against a backdrop of rising global demand, especially in the Asian and Middle Eastern markets. This means that even with a recovery in production in the US and growth in other markets, availability will remain tight, and prices will likely remain high, although perhaps not at today’s level.

For further insights, Rupert Claxton, Meat & Livestock Director, GIRA, is on this episode of the Beef Edge podcast discussing the global outlook for the beef industry. Listen in below:

Ireland is well placed to make use of its natural landscape to produce more beef, in a way that is both environmentally sustainable and, crucially from a market perspective, is commercially sustainable. This means that there are opportunities to invest in the Irish industry of the future, but that doesn’t mean maintaining the current structure. There must be some rationalisation of infrastructure to deliver efficiencies. This includes a reduction of slaughter capacity, a continuation of the scaling up of the breeding farms and an increase in specialised finishing.

The outlook for beef demand is good, but not without challenges; further alignment between producers and slaughter groups can be expected. The challenge now is to create an environment for investment at farm level, so that the profitability of 2025 can be reinvested in the industry for the future.

For more insights from the Teagasc National Beef Conference, visit here.

More from Teagasc Daily: Winter feeding: Get your cows breeding earlier next year

More from Teagasc Daily: Myostatin: The benefits and drawbacks