Market outlook for Irish beef and livestock, summer 2026

Summary

- Irish cattle prices have fallen by almost €0.70/kg since the beginning of the year and more than €1.00/kg since summer 2025.

- Domestic cattle prices have also fallen in the United Kingdom (UK) and continental European Union markets.

- In 2026, cattle supplies have fallen by 11% to-date, although some recovery is foreseen for the second half of the year.

- Irish beef exports to the UK market have fallen by more than 10%, partly because of strong competition from Australia and New Zealand in the wholesale and foodservice sector.

- Retail beef sales have also been impacted by price-conscious shopper behaviour, including switching to cheaper protein sources.

Producer price developments

The year 2025 will be remembered fondly by most beef farmers, as Irish cattle prices reached new record levels, rising by an average of 39% year-on-year. Unfortunately, however, producers have experienced considerable downward pressure on the value of their animals over recent months, and many are questioning whether there are any signs of stability appearing in the trade.

Most recently (week-ending 24 May), the average price of R-grade steers averaged €6.53/kg (excluding VAT) at Irish meat plants, which represented a decline of €0.09/kg from the previous week. These latest prices are €0.68/kg behind where they were at the beginning of the year (€7.21/kg), and €1.01/kg below where they were during the same week in 2025 (€7.54/kg).

Domestic cattle prices have also fallen sharply in our key export markets. The latest R- grade steer price in the UK has declined to the equivalent to €6.93/kg. Likewise, the European beef trade has experienced price pressure, with the European Union (EU) average R-grade young bull price dropping to €6.57/kg for the most recent week.

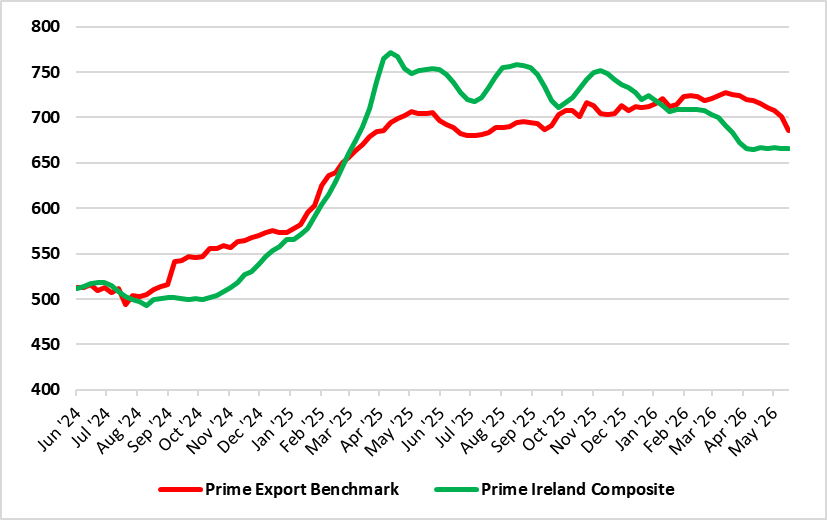

Each week, Bord Bia publishes its beef market tracking, which includes a comparison between the prices paid for prime cattle in Ireland against a weighted aggregated value accounting for six of our most important export destinations: namely the UK, France, Italy, Germany, the Netherlands, and Sweden. Effectively, the Export Benchmark represents the average price that Irish farmers would theoretically receive, if their cattle were priced according to the prevailing carcase prices in those countries. The differential between the Irish Prime Composite Price (€6.60/kg) and the Export Benchmark Price (€6.86/kg) has narrowed considerably (to €0.26/kg) over recent weeks. In mid-April, this differential was more than €0.50/kg, whereas this time last year the Irish price exceeded the Export Benchmark by more than €0.50/kg.

Figure 1. Comparison of Prime Irish Composite and Prime Export Benchmark Prices (cent/kg), from Bord Bia Beef Market Tracking

Irish beef exports

The value of Irish exports of primary beef reached €843 million for the first quarter of this year, which represented an increase of 9%, despite volumes falling by 7% to 114,000 tonnes in-line with lower production. The volume of exports to the UK market declined by 10 %, to 51,000 tonnes, reflecting competitive pressure in the foodservice sector especially. Meanwhile, exports to continental European markets were relatively more stable, dropping by 7% to 57,000 tonnes. Therefore, proportionally the EU accounted for 50 % of export volumes during the period (up from 47% in 2025), and the UK just 45% (down from 47% in 2025), while there was a notable decline of 24% in beef exports to international markets which were just 6,000 tonnes (5% of total).

Cattle and beef supplies

Irish cattle throughput has reached 647,626 head for the year to the week-ending 24 May. This represents a decline of 79,511 head, or 11%, from the strong levels recorded in the corresponding period in 2025. Some of this impact has effectively been offset by a notable improvement in average carcase weights. For the first four months of 2026, steer carcases were 22.9 kg, or 6.8%, heavier, on average, than the previous year, while heifers were 16.1 kg, or 5.4% heavier. Higher prices, improvement in genetics and slightly older average age at slaughter all contributed to this performance. Recent analysis of the Department of Agriculture’s Animal Identification and Movements (AIM) database suggests that cattle availability is likely to recover in the second half of 2026, with a somewhat more normal seasonal supply pattern returning compared with the very low levels of autumn 2025.

Across the EU, beef production is forecast to contract by 4.2% this year, according to the latest analysis by the European Commission. This follows a decline of 4.2% in 2025, which was partly attributable to the knock-on impact of Bluetongue disease on herd fertility and calf survival in several member states, alongside other sectoral challenges including regulatory requirements and generational renewal. The relative scarcity of EU beef is likely to be partly offset by an expected increase of approximately 10% in beef imports from outside the community, which follows an 18% increase in 2025, including gains of 30% for Brazil and 21% for Argentina.

UK market situation

In the UK market, domestic beef production has been largely stable so far this year. While there have been reductions of 0.5% and 6.5%, respectively, in the number of cattle slaughtered in Britain and Northern Ireland, this has been largely offset by slightly heavier carcase weights. What is more significant, however, has been the changing profile of beef imports into the UK over the past year. Under post-Brexit trade deals, Australia and New Zealand were allocated considerable tariff-free quotas, which has seen both countries significantly grow their share of the UK’s beef import volume, to 8% and 13%, respectively, in 2025. This product has been particularly prevalent in the lower to mid-tier UK foodservice sector, where commitments around country of origin are less clear, and sourcing decisions are based primarily on pricing and margins.

Figures for the first quarter of 2026 show that Ireland’s share of the UK’s beef import volume (fresh and frozen) fell from 77% to 64%, as a result of both the increasingly price-competitive nature of the foodservice market, but also economic difficulties contributing to more price-conscious shopper behaviour including switching to cheaper protein sources. IGD’s ShopperVista report for April 2026 shows that food prices are now the leading concern for 94 % of British shoppers.

Retail beef sales

The latest shopper data from Numerator in Britain shows that in the 12 weeks to the 19 April 2026, purchases of primary beef products fell by 8.8% in volume terms, as average prices rose by 18.5% to Sterling £12.33/kg. All the main beef products recorded lower volumes, with declines of 6.2% for mince, 9.9% for roasting joints, 10.1% for burgers and 10.9% for steaks.

Promotional focus

Bord Bia’s marketing plans for Irish beef in 2026 include targeted advertising and online activity in markets such as Britain, Italy, the Netherlands and Belgium, to reinforce Ireland’s strong reputation and encourage greater shopper engagement, based on the recognised quality of Irish beef produced under the Sustainable Beef and Lamb Assurance Scheme. Over the coming months, Bord Bia will also support several promotional campaigns in partnership with key export customers, along with organising numerous inward visits for important buyers and working with over 90 high-end chefs in our Chefs Irish Beef Club who act as passionate advocates in communicating the premium quality of Irish beef across nine key markets globally.

Live cattle trade

Trading of live cattle to European and international markets continues to represent a significant alternative outlet and an important source of competition for certain categories of stock, including dairy-bred calves and suckler-bred weanlings. Up to the 24 May 2026, a total of 211,880 head of Irish cattle have been exported live, representing a 15% decline on the same period in 2025. However, levels remain very similar to the corresponding period in 2023 and 2024. Calves dominated the trade during the first five months of the year, accounting for more than 80% of animals shipped. The Netherlands, Spain and Italy continue to be the key destinations for Irish calves, while Italy, Spain, Greece and North Africa are the principal markets for Irish weanlings.

Outlook

Despite subdued demand for beef in Britain, and in the main EU export markets, there are some signs of stability returning, with historically low cattle production expected to continue in the second half of 2026. In Ireland, the difficult start to the 2026 grazing season is likely to delay the supply of cattle off grass compared with other years. In general, the summer tends to bring about a seasonal recovery in the consumption of manufacturing beef and barbequing products, as temperatures and weather conditions improve. Recent experience has shown that customers running promotions with Irish beef have achieved very positive results, highlighting its strong resonance and reputation with consumers.

Acknowledgements

The information summarised here is based on insights and analysis from Bord Bia’s overseas market offices along with officially published data including from the Department of Agriculture, Food and the Marine, the EU Commission, AHDB, Numerator UK and IGD.

Compiled and edited by Mark McGee and Paul Crosson, Teagasc, Grange Animal & Grassland Research and Innovation Centre, and first published in BEEF2026 – Driving Sustainable Performance, additional reading from BEEF2026 is available here.