The economic performance and the role for diversification on cattle farms in Ireland

Summary

- Irish beef farms demonstrated a competitive position equivalent to the average of all EU-27, based on cash costs of production, with costs as a percent of output equivalent to the EU average.

- Despite this, economic viability levels have remained an issue in the drystock sectors, with some welcome respite in 2025.

- Given the economic competitiveness issues identified within Ireland, it is interesting to examine alternative diversification opportunities.

- Cattle farms with average levels of economic performance have the capacity to increase their economic returns by supplying perennial ryegrass-red clover silage for an anaerobic digestion (AD) plant.

- Decisions relating to renewable energy investment at farm level go beyond simple cost-benefit calculations, reflecting broader issues around trust, risk tolerance, policy instability, infrastructure, and generational transition.

Farm incomes are generally low on cattle farms in Ireland with farm subsidies accounting for the majority of farm income. Cattle farmers have contended with several economic challenges in recent years, with some welcome respite in margins in 2025. In this paper, Teagasc National Farm Survey (NFS) data is used to describe recent trends in farm income and competitiveness, and to explore the potential of anaerobic digestion (AD) feedstock supply as a potential diversification opportunity.

Farm income

Family Farm Income (FFI) represents the return to family farm labour, capital and land and is the principal measure of farm income used in the Teagasc NFS. In calculating farm income statistics, we distinguish between two main cattle systems i.e. Cattle Rearing and Cattle Other, (note: both systems exclude small farms i.e. farms with output of less than €8,000). The Cattle Rearing system includes farms concerned mainly with suckler cow farming and there are approximately 16,000 farms in this system. The Cattle Other system comprises of farms involved in the purchase of cattle (various ages) and the sale of store cattle in the marts or finished cattle to the factories, with approximately 35,000 farms in this system. Some farms in both cattle systems maintain a sheep or crop enterprise in addition to their main cattle enterprise. In 2024, the average FFI on the Cattle Rearing system was €13,862 per farm. The average FFI on the Cattle Other system was €18,141per farm. For 2025, we have estimated a 127% increase in average FFI on Cattle Rearing farms and a 26% increase on the Cattle Other farms.

Economic viability comparison across farming systems

The latest available data on economic viability of farming systems in Ireland is reported based on the Teagasc NFS for 2024. A farm business is defined as being economically viable if FFI is sufficient to remunerate family labour at the minimum wage in 2024 (which is assumed in this instance to be €22,860 per labour unit) and provide a 5% return on the capital invested in non-land assets, i.e. machinery and livestock. Farms that are found not to be economically viable but have an off-farm income source within the household (i.e. either the farmer or spouse are employed off-farm) are considered to be economically sustainable. Farm households are considered to be economically vulnerable if they are operating non-viable farm businesses and neither the farmer nor spouse have an off-farm job.

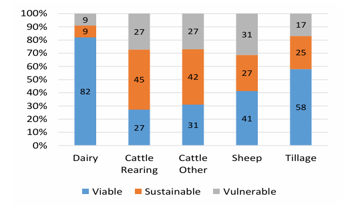

The viability of Irish farms varies across system. Figure 1 illustrates the wide differential between the viability of dairy and tillage farms, on average, compared to their drystock counterparts. In 2024, 82% of dairy farms were found to be viable, while only 9% of dairy farms were considered vulnerable. The situation on drystock farms was more challenging, particularly on Cattle Rearing farms where only 27% were deemed viable in 2024. The proportion of Cattle Rearing farms considered sustainable in 2024 was 45%, and 27% of Cattle Rearing farms were classified as vulnerable in 2024. Just below one-third (31%) of Cattle Other farms were classified as viable in 2024, whilst the share of Cattle Other farms deemed to be sustainable was 42%, with a further 27% vulnerable. Due to the estimated increases in farm incomes, it is expected that a significantly higher proportion of cattle farms will be deemed economically viable in 2025 compared to 2024.

Figure 1. Economic viability of farming by farm system, 2024. Source: Teagasc NFS

Competitiveness of cattle farms in Ireland

In evaluating the competitiveness of Irish cattle farms, data analysis was confined to the specialist cattle farms, based on the principal type of farming, and a gross output as defined by the Farm Accountancy Data Network (FADN). The competitive position of Irish farms was compared against all farms within the FADN dataset, and the European Union (EU-27) average, based on the most recent data from 2023.

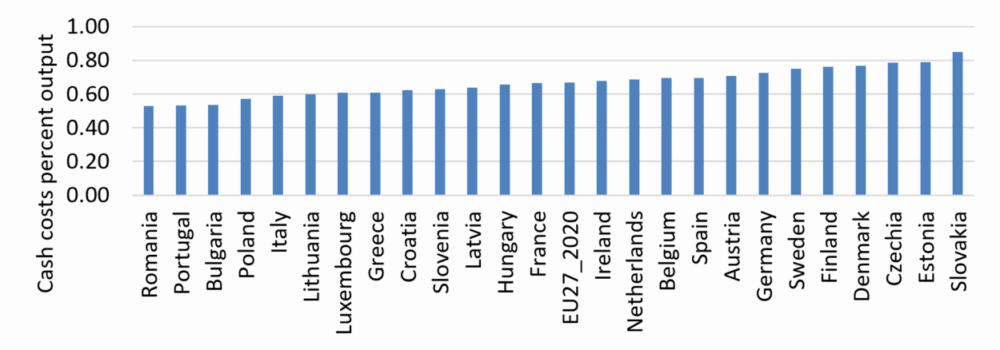

A number of cost and return-based indicators of competitiveness were examined for beef systems: costs as a percentage of output, margin over costs per hectare and margin over costs per livestock unit (LU). Overall, these results for beef rearing and fattening enterprises show that Irish producers performed with average levels of competitiveness within the EU, with cash costs as a percent of output value equivalent to the EU-27 average (Figure 2). However, it is important to note that when total economic costs (which includes an opportunity cost for owned resources land, labour and capital) were considered, Ireland’s competitive position worsens.

Figure 2. Costs as a percentage of total output (incl. subsidies) for European specialist cattle farms, 2022/2023. Source: Author’s estimate based on EC FADN data, 2022/2023.

Anaerobic digestion (AD) feedstock supply as a diversification opportunity

Given the economic competitiveness issues identified for cattle farms within Ireland, in terms of comparative economic viability measurements, it is interesting to examine alternative diversification opportunities. In particular, various EU and Irish policy documents identify a role for bioenergy to reduce greenhouse gas (GHG) emissions from agriculture and energy production. Furthermore, Ireland’s Climate Action Plan increased the target for anaerobic digestion (AD) to 5.7 Terawatt-hours (TWh) biomethane, recognising the role AD can play in reducing emissions and creating a circular bioeconomy.

The Sustainable Energy Authority of Ireland (SEAI) funded FLEET project (Farm Level Economic, Environmental and Transport Modelling of Feedstock Solutions) delivered a comprehensive assessment of the economic viability, environmental impact, and logistical challenges involved in using grass and animal waste as a feedstock for biomethane production at a national scale. The report finds that while supplying perennial ryegrass-red clover silage to AD plants can be a competitive alternative to traditional cattle and sheep enterprises, profitability varies significantly by farm and depends heavily on the price paid to farmers for silage. A survey conducted as part of the study revealed a strong willingness among farmers to supply 175,000 hectares of silage, well above the 110,000 to 130,000 hectares estimated to be required to meet Ireland’s 5.7 TWh biomethane production target for 2030. The study also highlighted significant environmental benefits to increased AD adoption. Grass-based AD feedstock systems could reduce farm-level GHG emissions by 50 to 98% per hectare on participating farms, driven largely by reductions in livestock numbers. Slurry-based AD feedstock systems were found to deliver emissions reductions as high as 11% per hectare.

A spatial transport analysis included in the study using national road network data indicates that, under non-constrained typical conditions, most AD feedstocks could be sourced within 10 km of potential AD plant locations. Under more constrained conditions, this range could extend to 15 km or more, with implications for both the associated cost and the emissions reductions achieved. At the national level, the development of a biomethane industry using grass silage and animal slurry to meet the 2030 target is projected to increase agricultural sector income by 1.2% to 1.3% (€49–€53 million) and reduce agricultural GHG emissions by 2.3% compared with a scenario where such feedstock use does not occur.

Solar energy production at farm level as a cost mitigation and diversification opportunity at farm level

As part of an SEAI funded project “Engagement Levels of the Farming Sector in Renewable Energy and Bioeconomy Projects” a study was conducted on the techno-economic and environmental feasibility assessment of grid-connected solar PV systems. The sensitivity analysis identified solar irradiance, grant funding, and grid electricity price as the most influential factors affecting financial performance. Further qualitative analysis conducted through a semi-structured interview approach, across all farm systems including on cattle farms, looked at farmers engagement levels with renewable energy and explored the drivers/benefits but also the barriers and challenges to engagement. The study highlights the multifaceted and interrelated financial and non-financial barriers/challenges and driver/benefits that Irish farmers face when considering investment in renewable energy initiatives. These go beyond simple cost-benefit calculations, reflecting broader issues around trust, risk tolerance, policy instability, infrastructure, and generational transition. Further research findings on this collaborative research project between Teagasc and Maynooth University is forthcoming.

Conclusion

Overall, the analysis shows that economic viability continues to be an issue within the drystock sector in Ireland and particularly for Cattle Rearing farms with these farms predominantly containing a single suckling enterprise. Whilst Irish producers demonstrated an average level of competitiveness in terms of cash costs when compared with other European countries, this position deteriorates when all opportunity costs are applied to all owned factors of production.

Given the economic competitiveness issues identified within Ireland, it is interesting to examine alternative diversification opportunities. Results show that cattle farms with average levels of economic performance have the capacity to increase their economic returns by supplying grass silage for an AD plant. At the national level, the development of a biomethane industry using grass silage and animal slurry to meet the 2030 target is projected to increase agricultural sector income by 1.2% to 1.3% (€49–€53 million) and reduce agricultural GHG emissions by 2.3% compared with a scenario where such feedstock use does not occur. Finally, in relation to renewable energy investment at farm level, research has shown that investment decisions go beyond simple cost-benefit calculations, reflecting broader issues around trust, risk tolerance, policy instability, infrastructure, and generational transition.

Acknowledgements

The authors acknowledge the contributions of colleagues Brian Moran, John Lennon and the Teagasc NFS recorders in collecting and validating the Teagasc NFS data. The authors are most appreciative to the farmers for their participation in the Teagasc NFS. The authors gratefully acknowledge the SEAI and GNI for providing research funding for the FLEET project and ‘The Engagement Levels of the Farming Sector in Renewable Energy and Bioeconomy Projects as part of the RD&D programme.

Compiled and edited by Mark McGee and Paul Crosson, Teagasc, Grange Animal & Grassland Research and Innovation Centre, and first published in BEEF2026 – Driving Sustainable Performance, additional reading from BEEF2026 is available here.