An overview of beef cattle farming in Ireland

Summary

- Beef farming in Ireland, derived from the progeny and unproductive animals of the suckler and dairy cow herds, makes a crucial contribution to agricultural output and exports.

- Beef farm incomes have increased considerably in recent years, although volatility in input and cattle prices has created some challenges.

- Operating technically efficient beef systems is key to maximising profitability and building resilience to market volatility.

- An online survey of beef farmers highlighted the importance of off-farm employment, the issue of succession and the focus on improving labour efficiency.

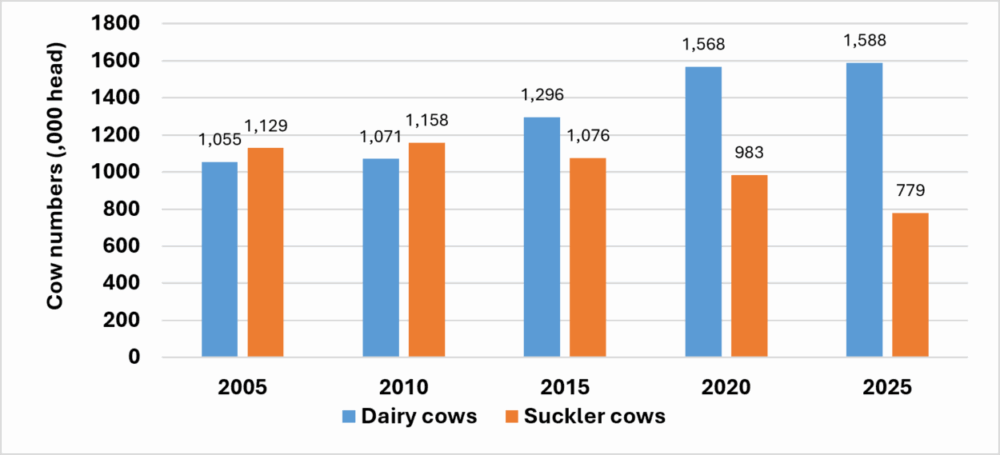

From the perspective of farm numbers and land area farmed, beef cattle farming is the most important agricultural enterprise in Ireland. Moreover, the sector contributed €4.2 billion, some 30%, to total agricultural output in 2025, an increase of €1.1 billion when compared to 2024. The beef sector is export orientated with over 90% of production exported at a value of €3.6 billion in 2025. Beef cattle are sourced from the suckler beef and dairy herds. There has been a sizable change in the respective national herd sizes in the past 20 years (Figure 1). There were approximately equal numbers of each in 2005, whereas the number of dairy cows is now more than double that of suckler cows. This of course, has implications for systems operated on farms with more beef farmers rearing dairy-beef progeny (Further information: Profitable pasture-based dairy-beef systems).

Figure 1. Number of suckler and dairy cows in Ireland. Source: CSO, June Census

Two key challenges facing the sector at farm level are profitability and generational renewal. To some extent both are related given that a key question for any potential farm successor is, can the farm financially support a family and/or provide a reasonable return for labour and resources employed on the farm? In this paper, we will assess the financial performance of beef farms in Ireland particularly given the recent volatility in beef markets, and the broader question of generational renewal and future farm planning based on a recent survey of over 300 beef farmers.

Farm incomes

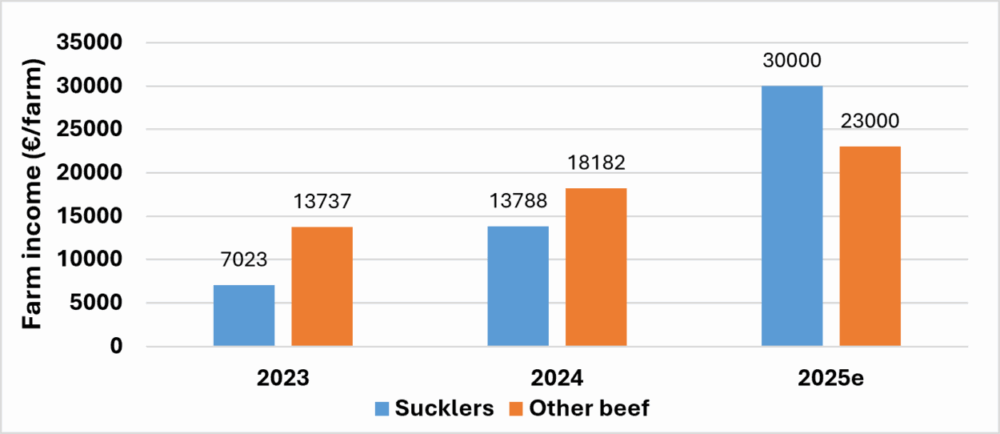

The beef sector is characterised by relatively small (~30 hectares (ha) / 80 acres), albeit with large variation, family farms with a broad geographical distribution. Given this scale, profitability within the sector has been challenging (Figure 2) and off-farm employment provides an important source of income for family farms. Indeed, more than half of all beef farmers have off-farm income and in many cases the spouse is also employed off-farm.

Figure 2. Farm incomes for suckler and ‘other beef’ farms in 2023, 2024 and 2025. Source: Teagasc REDP

There are two points worth making in relation to farm incomes. Firstly, incomes have increased very considerably in recent years largely due to the increase in beef price which is discussed later in this paper. Estimates for 2025 indicate that suckler farm incomes have more than doubled when compared to 2024, which were, in turn, more than double that achieved in 2023. Other beef farms (i.e. non-suckling beef farms) also saw very large income increases. Secondly, average incomes mask the enormous variation in incomes on beef farms. It is extraordinary that, the bottom third of farm incomes in 2025 were less than the top third in 2024 despite the generational increase in cattle and beef prices (Table 1). It is very apparent that, although price is the key driver of farm profitability, technical efficiency has a major bearing on overall performance.

Table 1. Financial performance (€/hectare) of beef systems stratified by profitability in 2024 and 2025

| 2024 | 2025 | |||||

| Top third | Middle third | Bottom third | Top third | Middle third | Bottom third | |

| Sucklers | 520 | 96 | -284 | 1579 | 709 | 223 |

| Other beef | 808 | 191 | -167 | 1132 | 339 | -80 |

Implications of price volatility on the margin from various beef production systems

As noted above, the beef sector has witnessed unprecedented price volatility in recent years. As indicated in Figure 3, the period from June 2013 to the start of 2022 saw beef prices remaining relatively stable, ranging from ~€3.40/kg to €4.40/kg. Subsequently, beef prices rose sharply from €4.30/kg to €7.73/kg in mid-2025. While there have been price declines in the first half of 2026, the indications are that prices are stabilising at a level in excess of those which prevailed before the recent period of volatility. An overview of the recent beef moves and insights into the market factors underpinning these price changes is provided elsewhere (Further information: Market outlook for Irish beef and livestock, summer 2026).

Figure 3. Beef prices (R3 prime, €/kg exc VAT) for Irish (steers, green line), UK (steers, blue line) and European (young bulls, red line) from June 2013 to May 2026. Source: Bord Bia

Weanling and calf prices broadly reflect the prevailing beef price at a given point in time such that when beef prices are rising, weanling (and calf) prices tend to rise accordingly and vice versa. Thus, the recent fluctuations in beef price have seen weanling prices vary hugely in this same time period (Table 2).

Table 2. Prices paid (€/kg live weight) for weanling progeny from late-maturing breed suckler cows and sires sold at livestock marts in Ireland for the years 2024, 2025 and 2026 (to 20 May 2026).

| 2024 | 2025 | 2026 (to date) | |||||||

| Bottom 25% | Average | Top 25% | Bottom 25% | Average | Top 25% | Bottom 25% | Average | Top 25% | |

| Bulls | 2.87 | 3.13 | 3.38 | 4.10 | 4.60 | 5.08 | 4.56 | 5.01 | 5.45 |

| Heifers | 2.78 | 3.08 | 3.30 | 4.06 | 4.58 | 5.05 | 4.52 | 4.96 | 5.35 |

| Source: Author’s analysis based on ICBF data | |||||||||

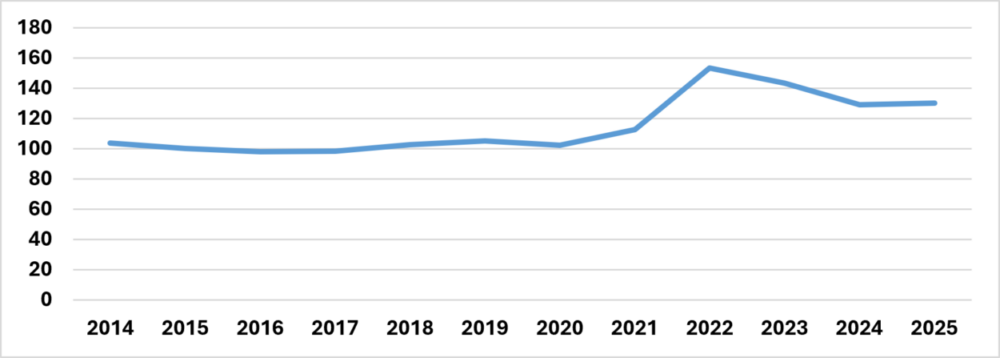

Input prices have shown similar levels of volatility following a period of relative stability (Figure 4) rising to a peak following the inflationary effect of the post-Covid period, which was exacerbated by the impact of the Russian invasion of Ukraine. Input prices have reduced from those peaks, although the effect of the current conflict in the Middle East has again led to inflationary pressures. This resulted in the hugely changeable beef farm incomes in recent years alluded to previously.

A challenge as regards interpreting the implications of these prices on farm level profitability is that farmers operate a very wide range of production systems and the production cycle of beef farm systems straddle several years. For example, a beef carcass price increase is likely to give rise to an increase in weanling (or calf) prices in that same year. The overall effect for that year can be positive or negative depending on; (1) the production system operated, (2) the extent of this ‘capitalization’ of beef price into live animal prices, and (3) any changes in input prices.

Figure 4. Agricultural input price index (2015 = 100). Source: Central Statistics Office (CSO)

Suckler cow farmers selling weanlings directly benefit from price increases with an additional benefit being the increase in cull cow value. Weanling-to-beef farmers benefit from the beef price increase in the finishing cattle they sell, but this is (partially) offset by the higher price they must pay for weanlings for the next production cycle. The same principle applies for dairy calf-to-beef production systems. The multi-year nature of these weanling-to-beef production systems must also be considered. If the beef price remains elevated, the higher price paid for weanlings in the preceding year by weanling-to-beef farmers will be compensated for in the value of the animal at sale; however, if beef price declines, the higher weanling price may lead to a loss-making situation for that production cycle, although not necessarily in that particular year if weanling prices in that year also decline as would likely be the case. To explore this further, four scenarios based on the beef and weanling prices which prevailed in the 2024-2026 period (Figure 3 and Table 2) and the beef systems analysis presented elsewhere (Further information: Suckler beef systems for profitable production and Growing-finishing beef cattle: national performance data and growth targets) were developed (Table 3).

Table 3. Effect of weanling and beef price volatility on the net margin (per hectare (ha) and per animal sold) for a range of contrasting suckler production systems1

| Beef price (€/kg carcass weight) | High | High | Low | Low | Range |

| Weanling price (€/kg live weight) | Low | High | Low | High | |

| Net margin (€/ha) | |||||

| Suckler weanling system | 695 | 1638 | 504 | 1447 | 1133 |

| Weanling-to-beef system 1 | 3678 | 1018 | 519 | -2141 | 5819 |

| Weanling-to-beef system 2 | 3037 | 980 | 500 | -1557 | 4595 |

| Weanling-to-beef system 3 | 2313 | 801 | 394 | -1117 | 3429 |

| Net margin (€/animal sold) | |||||

| Suckler weanling system | 451 | 1063 | 327 | 939 | 736 |

| Weanling-to-beef system 1 | 856 | 237 | 121 | -498 | 1355 |

| Weanling-to-beef system 2 | 916 | 296 | 151 | -469 | 1385 |

| Weanling-to-beef system 3 | 951 | 330 | 162 | -460 | 1411 |

| 1High-beef price, €7.53/kg carcass. Low-beef price, €5.43/kg carcass. High-weanling price, €4.99/kg live weight. Low-weanling price, €3.11/kg carcass. Weanling-to-beef system 1, finishing steers at 20 months of age and heifers at 19 months of age. Weanling-to-beef system 2, finishing steers at 23 months of age and heifers at 19 months of age. Weanling-to-beef system 3, finishing steers at 27 months of age and heifers at 19 months of age. | |||||

This analysis indicates the impact of recent volatility on the net margin of alternative beef production systems. Although the highest margins were obtained for the weanling-to-beef systems, average margin was greatest for suckler weanling system and the range in profitability was lowest. Essentially, suckler weanling systems tend to be insulated to a greater extent from recent price fluctuations; however, it is worth pointing out that, over the longer term, suckler weanling farms have tended to generate the lowest income among beef farming systems.

Generational renewal and future plans of Irish beef farmers

The issue of generational renewal is dealt with elsewhere in these proceedings (Further information: Farming for the next generation). To gain a better understanding of farmers’ views in relation to generational renewal and succession, Teagasc carried out an online questionnaire survey of beef farmers in May 2026. A total of 303 farmers with a very broad geographic distribution responded to the survey, the majority of whom were Teagasc clients. While this survey is not strictly representative of the entire beef farming population, it provides valuable insight from a large cohort of beef farmers into current practices on Irish beef farms, particularly in relation to labour efficiency, succession and future investment plans.

Off-farm employment and labour

Taking up off-farm employment has become an increasingly common way to supplement beef family farm income. This long-term trend has important implications for the total number of hours farmers are working each week and is likely to shape the level of production the next generation are willing to commit to. Almost two-thirds (63%) of respondents to the survey had an off-farm job, which is somewhat greater than the national average of 47% for suckler farmers and 55% for non-suckler beef farmers. Of these 63%, 81% worked at least 30 hours per week off-farm. The age profile also differed between part-time and full-time beef farmers. Overall, 76% of respondents were between 35 and 69 years of age. However, among part-time farmers, 51% were aged between 35 and 54, while 55% of full-time farmers were aged between 55 and 69. This indicates that, as expected, full-time beef farmers tend to be older than those who also work off-farm.

Part-time farmers reported working an average of 25 hours per week on the farm, which is a significant commitment. In addition, part-time farmers used an average of 14 days of holiday time from their off-farm employment to carry out farm work. Seventy-six percent of respondents said that family members regularly help them with work on the farm. The time pressures faced by beef farmers were further highlighted by the fact that 48% said they do not regularly take part in a hobby or sport. Of these, 65% said this was because they do not have the time.

The survey also looked at the use of paid labour on beef farms, with 82% of respondents saying they used some form of paid help. However, for almost two-thirds of these farmers, this amounted to less than 150 hours per year. Labour availability was also an issue, with almost one third saying it was difficult, or almost impossible, to get someone to carry out part-time work on the farm. Nearly all the survey respondents said they used contractors to varying degrees. However, while part-time farmers do use contractors or hired labour slightly more than full-time farmers, the difference was not as great as one might assume. Farmers with an off-farm job selected an average of 5.6 contractor jobs, compared with 5.3 jobs for those without an off-farm job although the total hours completed by contractors compared to the farmers’ own labour was not specified.

Succession

Succession was another important area covered in the survey. When asked who might take over the family farm in time, 61% of respondents said this was a relevant question for them. However, within this group, a relatively high proportion, 25%, said they had not yet identified a potential successor. When asked whether they had taken any formal steps in relation to succession planning, a further 25% said they had not. Among those who had taken steps, these included discussing succession with family members, seeking legal and tax advice, and, in some cases, putting a formal transfer plan in place.

Interestingly, 16% of farmers who completed the survey said they were already involved in a registered farm partnership. This is an encouraging finding, as registered farm partnerships are still a relatively recent development on Irish farms and are often more closely associated with dairy farming than with beef systems.

Farm system changes; past and future

Of those who completed the survey, 67% said they currently keep suckler cows. The average herd size among these respondents was 31 cows. Among farmers who do not currently have suckler cows, 18% said they had kept cows within the past five years. In general, these farmers had exited suckling because they viewed it as a labour-intensive enterprise that was becoming increasingly difficult to justify or manage, particularly alongside off-farm employment. This suggests that suckler cows may be particularly vulnerable on farms where available family labour has reduced, or where the farmer is increasingly dependent on off-farm employment.

Among farmers who currently keep suckler cows, 87% said they expect to still have cows in five years’ time. Within this group, 27% said they expect to have more cows, while 14% expect to have fewer. A further 12% were unsure whether their cow numbers would remain the same as they are today. Where farmers said they did not expect to still have suckler cows in five years’ time, more than half cited age, retirement, or plans to lease the farm as their main reason. The next most common reasons were labour, workload, time requirements and lifestyle. Comments such as “a lot of work” and “to free up time” suggest that suckler production is often viewed as a demanding enterprise when compared with other farming or lifestyle options.

Dairy cow numbers have increased substantially in recent years (Figure 1) and, as a result, over the past decade, many farmers have introduced or expanded their dairy calf-to-beef systems. Of those who completed the survey, 35% said they rear dairy-bred calves. The average number reared by these farmers was 68 calves per year. Among those who do not currently rear dairy-bred calves, 17% said they had done so within the past five years but have since stopped. For these farmers, 42% referred to the cost of calves, poor returns, or better value from alternative systems. The next most common reasons related to labour, time and workload.

Among farmers currently rearing dairy-bred calves, 96% said they expect to still be rearing calves in five years’ time, with very few planning to stop. One-third, 33%, expect to rear more calves, while 58% expect to rear the same number. There was little indication from the survey that farmers intend to reduce the number of calves they purchase.

Another important group of beef farmers are those who buy in weanlings, yearlings, stores or ‘runners’ and may or may not have suckler cows or rear dairy-bred calves. Thirty-seven percent of the farmers in the survey said they bought these types of cattle and 38% of these said they had changed the type of cattle they have bought in over the last five years. The main reason for changing was economic pressure, particularly the rising purchase price of cattle and the search for better value or improved returns. A second important pattern was a move towards cattle that could be finished earlier, kept for a shorter period or turned over more quickly.

Investing in labour efficiency

Improving labour efficiency has become an important focus on many beef farms. Investment in better handling facilities, housing, machinery and other labour-saving measures can make farms safer, easier and more attractive places to work. This is particularly important where farmers are also working full-time off-farm, or where the next generation may only be willing to continue farming if the workload is manageable.

Seventy percent of survey respondents had invested in their farms over the last five years to make them more labour efficient. The most frequently cited investments were cattle handling facilities, machinery, sheds and housing, and fencing or grazing infrastructure. These investments appear to be motivated by a desire to reduce physical workload, improve safety and allow routine livestock tasks to be carried out by fewer people. Investments relating to calving and calf rearing were also prominent, including automatic calf feeders, calving pens and monitoring cameras. Although some farmers adopted digital technologies such as heat detection systems, herd apps and EID equipment, these were less common than physical improvements to farm buildings, machinery and livestock handling systems. Overall, the findings suggest that labour efficiency on beef farms is being pursued mainly through practical improvements that simplify daily work and reduce the need for manual handling.

Seventy-four percent plan on investing in labour efficiency on their farms over the coming five years. The most frequently identified priority was improved housing and farm buildings, including new sheds, slatted accommodation, calf and calving facilities and additional slurry storage. Cattle handling facilities, fencing, paddocks, water systems and roadways also remain important planned investments, particularly where they allow routine stock management to be carried out safely by one person. Like the investments made in previous years, future investment plans are focused on reducing manual work, improving safety, simplifying winter management and making farm operations less dependent on additional labour.

For the 26% of beef farmers who do not plan on investing in labour efficiency for their farms the results were very interesting. The most frequently cited reason was financial constraint, including cost, lack of finance, poor profitability and concerns about the return on investment. Age and retirement were also major factors, with many respondents indicating that they were approaching retirement, scaling back or did not consider further capital investment worthwhile at their stage of farming. Together, financial considerations and age or retirement accounted for over 60% of the written explanations provided. A further important group of farmers stated that they had already achieved sufficient labour efficiency, had previously completed the improvements they considered necessary, or could not identify further worthwhile changes. Smaller numbers referred to succession uncertainty, farm scale, unsuitable investment options or simply having no current plans to invest.

Building more sustainable beef systems

Thirty-five percent of respondents said they had made changes to their beef farm in the last five years with a variety of answers and reasons provided. Financial performance was the most common primary driver of change, accounting for 32% of responses. Farmers referred to improving profitability, addressing high input and replacement costs. Labour and lifestyle considerations were also prominent, accounting for 28% of primary reasons and being mentioned in 38% of all responses. These farmers sought to reduce workload, save time, manage farming alongside off-farm employment, create more family time or adapt to ageing and health constraints. A further 23% primarily changed their system to improve efficiency, output, livestock quality or the overall direction of the farm enterprise. Smaller numbers referred to succession, partnership or land changes, TB and health problems, or organic conversion. Overall, the responses indicate that farmers are adapting their beef systems both defensively, in response to costs, labour shortages and personal constraints, and proactively, in pursuit of improved profitability, efficiency, expansion and long-term farm viability.

All respondents were invited to provide additional comments on labour efficiency, succession and future planning on beef farms. Three interconnected issues dominated the responses: farm profitability and income viability, labour and workload pressures, and succession or the ability to attract the next generation. Each of these issues was mentioned in approximately 40% of the substantive comments.

Farmers described low or volatile financial returns, an issue we highlighted previously in this paper, rising input and investment costs, and reliance on off-farm employment as major barriers to the future sustainability of beef farming. Labour was also a central concern, with respondents referring to difficulty sourcing help, high workload, lack of time off, reduced family time and the need for safer, simpler and less labour-intensive systems. Farmers identified improved facilities, labour-saving technology, better access to relief labour and practical management changes as potential solutions, but many stated that poor profitability restricted their ability to invest.

Succession was viewed as a major national and local challenge. Respondents referred to farms without identified successors, uncertainty about whether children would take over, delayed transfer by older farmers and the need for retirement incentives, transfer advice and greater encouragement for younger people. Many considered that succession would remain difficult unless beef farming could provide an acceptable income and quality of life.

Overall, the responses suggest that future planning for beef farms cannot focus on succession or labour efficiency in isolation. Farmers see profitability, manageable workload, investment capacity, retirement arrangements and the attractiveness of farming to the next generation as closely linked. Measures that improve returns, reduce labour burden, facilitate farm transfer and support farmer wellbeing are likely to be central to maintaining viable family beef farms in the future.

Environmental sustainability

A key factor to consider in relation to beef farming is the impact of this activity on environmental sustainability. This is a consideration for food systems generally; however, there is particular scrutiny on livestock farming given its disproportionate requirement for land occupation and contribution to greenhouse gas emissions in the form of methane. Irish beef farming systems are based on permanent pasture and in this respect, plays a crucial role in converting non-human edible resources (forage) into high quality human food (beef meat). While one could argue that much of this land could otherwise be used for directly feeding people in the form of cereal crops, implications of such land use change for soil carbon loss and loss of natural grassland ecosystems would certainly mitigate against this argument from a broader sustainability perspective.

The issue of methane loss from enteric fermentation (i.e. the production of methane as a by-product of the microbial decomposition of feed material in the rumen of ruminant livestock) has been the focus of extensive research over many years. There is an ongoing debate about the manner in which methane gas is quantified in greenhouse gas emission accounting systems such as the national inventories which report to the Intergovernmental Panel on Climate Change. The short-lived nature of methane gas relative to many other greenhouse gases such as carbon dioxide and nitrous oxide is at the core of this discussion. Notwithstanding this wider debate, standard international frameworks are predominantly based on ‘GWP100’ which equates the heat-trapping potential of greenhouse gases to carbon dioxide over a 100-year period. In Ireland, international and EU commitments are mainly based on this metric. A further point to consider is that methane loss from enteric fermentation is an energetic loss from feed digestion in livestock and the reduction of this loss or redirection into productive energy use such as animal live weight gain is desirable. A summary of the very wide range of research studies which have set out to better quantify methane emissions from beef cattle production systems and to evaluate measures to abate such emissions, including methane mitigating feed additives, is presented elsewhere (Further information: Methane-reducing feed additive research in beef cattle).

Compiled and edited by Mark McGee and Paul Crosson, Teagasc, Grange Animal & Grassland Research and Innovation Centre, and first published in BEEF2026 – Driving Sustainable Performance, additional reading from BEEF2026 is available here.